March 12, 2026

Strategic Insights on Financing Solar and Storage in Today’s Capital Markets

Delivering bankability and sponsor confidence

Electricity consumption is increasing at a pace not seen in decades. Market outlooks forecast U.S. electricity demand growth of roughly 35% to 50% over the next 15 years, a sharp departure from the relatively flat demand era many stakeholders had grown accustomed to.

At the same time, energy buyers are under pressure to secure new supply that is affordable and timely. Electricity prices are rising in many regions, driven by accelerating demand from data centers and AI infrastructure. In critical markets such as PJM, new analysis indicates that without additional renewable generation, ratepayers across nine states could face an estimated $360 billion in additional electricity costs over the next decade.

In this environment, utility-scale solar and battery energy storage stand out. They are among the fastest resources to deploy, and the economics remain compelling even in a higher interest rate environment. Lazard’s June 2025 LCOE+ report makes clear that competitiveness of renewables from a levelized cost of energy is not dependent on subsidies. Even without tax incentives, wind and solar rank among the lowest-cost sources of new generation in the United States. The data-driven analysis expects renewables to play a central role in meeting rising power demand while helping contain long-term cost pressures.

Against that backdrop, Arevon’s Project Finance team sees two realities at once. The structural foundation of project finance remains sound. In a volatile market, it continues to serve as the most effective mechanism for channeling private capital into large-scale energy assets, provided the sponsor has the expertise to navigate risk and close transactions. At the same time, the market around that foundation is evolving quickly, with more participants in the capital stack, heightened scrutiny around policy and regulatory risk, and new dynamics shaping energy storage and solar-plus-storage hybrid projects.

Below is a practical look at how renewable energy projects are financed, how deal structures are evolving, and what financiers are scrutinizing most today.

The Foundation: How Project Finance Works

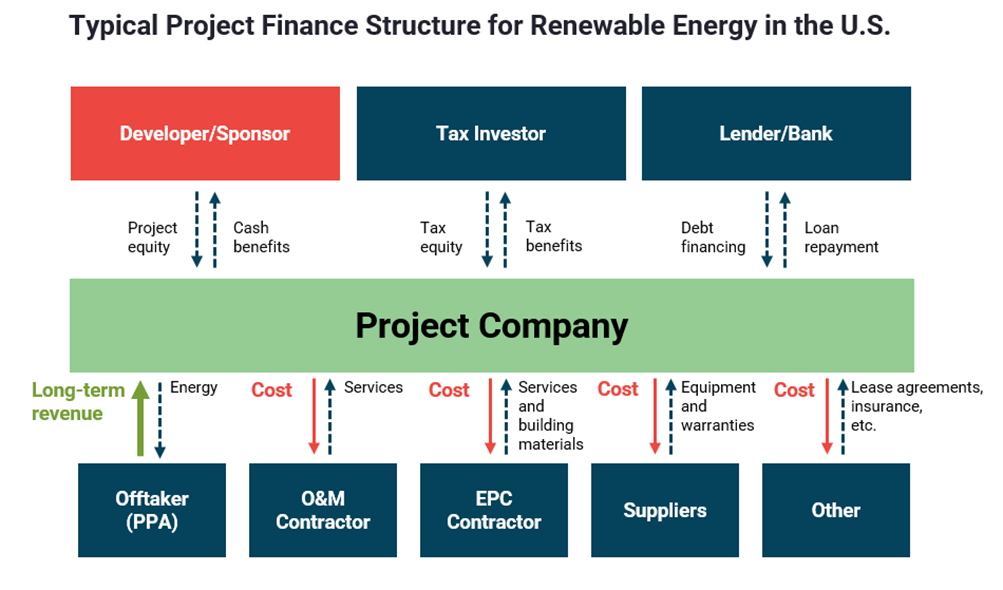

Project finance is the funding of long-term infrastructure projects using a non-recourse or limited recourse structure. Debt and equity are repaid primarily from the cash flow generated by the project itself. In a true non-recourse structure, lenders do not underwrite to the sponsor’s balance sheet. Their primary recourse is the project, its contracts, and its ability to generate stable revenue.

Upfront costs to build projects are significant, while long-term operating costs are relatively low and stable, especially because solar has no fuel cost exposure. That lack of fuel risk is increasingly valuable as geopolitical pressures push crude oil and natural gas prices higher and create volatility in global energy markets.

Project finance solutions can unlock low cost of capital funding to accelerate deployment of utility-scale renewable energy projects.

A typical structure includes three primary sources of capital:

- Sponsor equity

- Project-level debt

- Tax equity, where applicable

Each plays a distinct role. This structure also reflects a central concept in project finance: different stakeholders value different economic streams. A project’s value can include cash distributions, taxable income, and tax attributes linked to that income. Capital partners are brought in based on who values which stream most, with the goal of lowering overall cost of capital while still enabling the project owner to retain the long-term asset and the cash profile that supports its strategy.

As a privately held company, Arevon’s corporate investors provide sponsor equity that helps fund development and early-stage project work. Once a project reaches a point where it is clearly viable and ready to move forward, including site control, interconnection progress, and a contracted revenue stream such as a power purchase agreement, the company brings in third-party capital to fund the majority of construction costs.

This is also where the rigor of project finance becomes clear. While non-recourse lending can appear risky at first glance, renewable energy project finance is structured around extensive diligence and robust contractual frameworks. Lenders conduct deep technical, commercial, and legal diligence to validate the project’s ability to perform and generate the cash flows required to repay the loan. That level of scrutiny is one reason many in the market consider well-structured project finance to be one of the safer forms of infrastructure lending.

The Capital Stack in Practice

Renewable projects combine sponsor equity, debt, and tax-driven capital in proportions that vary by project, contracting, and technology. As a general reference point, Arevon’s projects often include a minority share of project equity, with the remainder funded through debt and tax equity. The exact mix depends on the offtake structure, the tax attributes available, and the risk profile the market assigns to the project.

Arevon also has a corporate debt facility managed by its treasury team. A corporate facility is a flexible line of credit supported by the strength of the overall business, rather than tied to a single project. It provides key advantages, including:

- Enabling speed and flexibility, including the ability to act quickly on procurement and safe harbor strategies when supply chain conditions shift.

- Reducing financing costs because lenders are underwriting a diversified platform rather than a single asset. That flexibility helps manage timing mismatches between development, procurement, construction, and permanent financing.

When Arevon borrows through a corporate facility to fund a project, that borrowed amount is effectively part of project equity.

Tax equity is a separate component. Many renewable projects generate tax attributes that the project owner may not be able to fully utilize. In those cases, third-party tax equity investors contribute upfront capital in exchange for receiving a share of tax benefits, typically paired with a smaller share of cash distributions.

In some structures, project-level debt is semi-permanent and sculpted to the length of the offtake agreement but matures earlier, creating a planned refinancing point after a project has established operating history. As the project de-risks through successful operations, it may be able to secure improved terms in a refinancing.

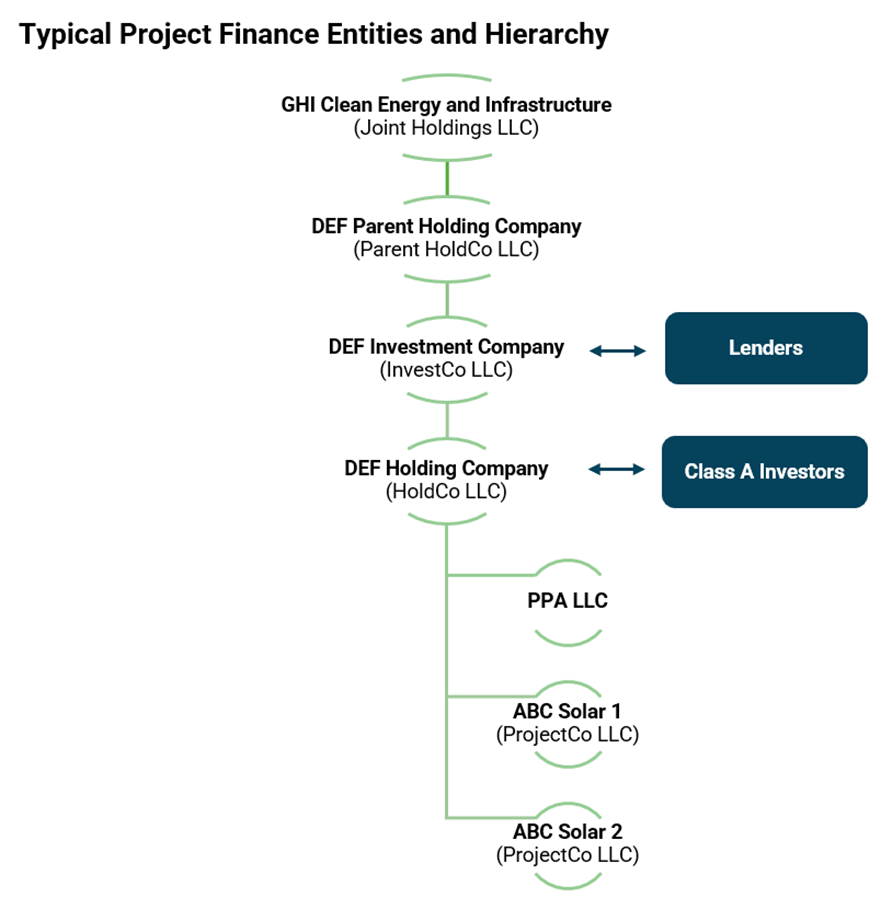

A typical project structure includes multiple entities designed to allocate risk appropriately among investors, lenders, and owners. Revenue flows into the project company through long-term agreements with offtakers. The project company also enters into engineering, procurement, and construction contracts, operations and maintenance agreements, land leases, equipment supply agreements, and a range of other commercial obligations required to build and operate the asset.

From a risk perspective, financing parties closer to the project’s contracted revenue streams are generally more insulated.

For Arevon, assembling this capital stack and coordinating among lenders, tax investors, and corporate stakeholders is a core competency of the finance team. It is how projects successfully move from concept to construction, and ultimately to long-term operation.

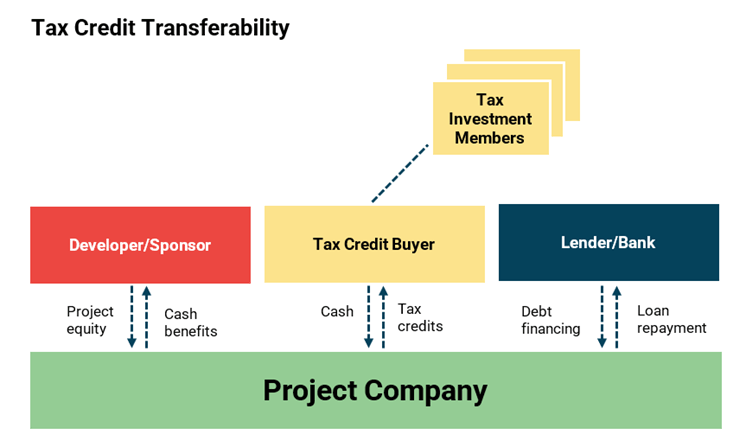

Transferability Expands Access to Capital While Adding Complexity

The Inflation Reduction Act introduced transferability, which continues to allow tax credits to be sold to third parties for cash once a project is placed in service. This tool can support development and construction liquidity and can be leveraged to retire short-term construction debt.

Transferability expands the market for tax credit monetization. At the same time, adding another participant to the capital structure increases complexity.

Historically, a project might have included a lender and sponsor equity. Then tax equity became common. With transferability, projects may include lenders, tax equity, and tax credit buyers, each with their own diligence requirements, documentation expectations, and risk allocation frameworks. More participants can mean more structuring work and longer timelines, even when the underlying project fundamentals are strong.

Sponsor Quality Matters More in an Uncertain Market

In today’s market, uncertainty is a defining challenge. It is not only the nature of individual policy decisions, but the difficulty of predicting what changes might occur and when.

Uncertainty can reduce depth of capital as participants step to the sidelines. It can also make capital more restrictive, with lenders and investors requiring tighter provisions to protect against change in law, tariffs, permitting risk, and other external factors.

In that environment, sponsor selection becomes central. Over a 30-year asset life, many unexpected events can occur. Financing parties, particularly banks that are not in the business of owning and operating assets, rely on the sponsor’s capability and track record to manage through volatility and protect the project’s value.

Nimmi Kavasery

Managing Director of Project Finance, Arevon

“Financing partners want to know who is steering the ship. I think what makes Arevon one of the best IPPs in the industry is the breadth and depth of expertise we bring across the platform, including interconnection, asset management, tax, engineering, and regulatory matters. We also have a well-established track record of owning and operating projects. The fact that we are long-term owners is important to financing partners because it gives them confidence that the sponsor responsible for building the project will also be there to manage it over its lifespan.”

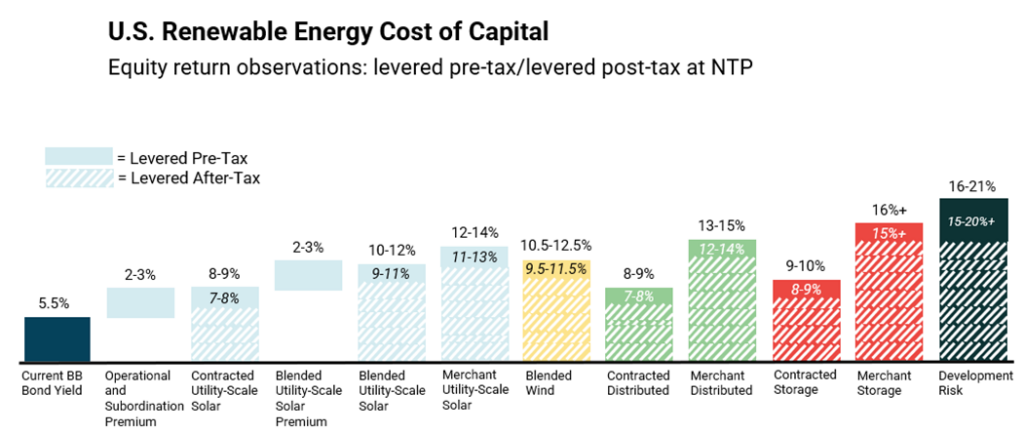

That dynamic also influences cost of capital. Sponsors with established platforms and operating track records generally have access to lower-cost capital, while newer developers often face higher financing costs. Large financial institutions can be selective about where they deploy capital, and in uncertain markets they tend to favor sponsors with proven execution, disciplined risk management, and the ability to navigate challenges over the life of the asset.

That preference shows up clearly in project economics. The level of risk investors assign to a project directly influences the cost of capital required to finance it.

Ines Serrao

Managing Director and Co-Head of U.S. Project Finance & Infrastructure, CIBC

“CIBC is proud to support Arevon, a leading independent power producer in North America. As a valued partner, our collaboration underscores our shared commitment to advancing the renewable energy sector while delivering innovative solutions for our clients. Together, we continue to support utility-scale solar and storage projects that enable a more sustainable economy.”

Risk Underwriting Is Evolving

All infrastructure projects carry core categories of risk that investors underwrite throughout the project life cycle: development risk, commercial risk including contracted versus merchant exposure, and operating and production risk.

Additional externally driven risks are now layered on top of what should be a project’s normal risk profile, including policy changes, supply chain disruption, and tariffs. These factors are now central to how lenders, tax equity investors, and sponsors evaluate transactions, and they are materially harder to predict and manage than the traditional development, commercial, and operating risks the market has underwritten for years.

One of the most difficult risks to underwrite is regulatory risk. These risks can disrupt construction schedules, raise costs, and could threaten offtake agreements if commercial operation dates are missed. They also drive up cost of capital.

In extreme cases, when financiers require sponsor support, the economics can shift. A parent guarantee moves what is intended to be project-level, non-recourse risk back onto the sponsor’s balance sheet. In those situations, a sponsor may determine that it is more efficient to use corporate debt, which can be lower cost than project finance debt, rather than provide balance sheet support to achieve a similar result.

Strong sponsors with flexible capital structures are therefore better positioned to move projects forward when markets tighten, which is one reason experienced platforms continue to attract institutional capital even during periods of volatility.

Competitiveness and Speed

The U.S. power system needs new supply. Demand growth and electrification trends are pushing buyers to secure resources that are affordable and deliverable.

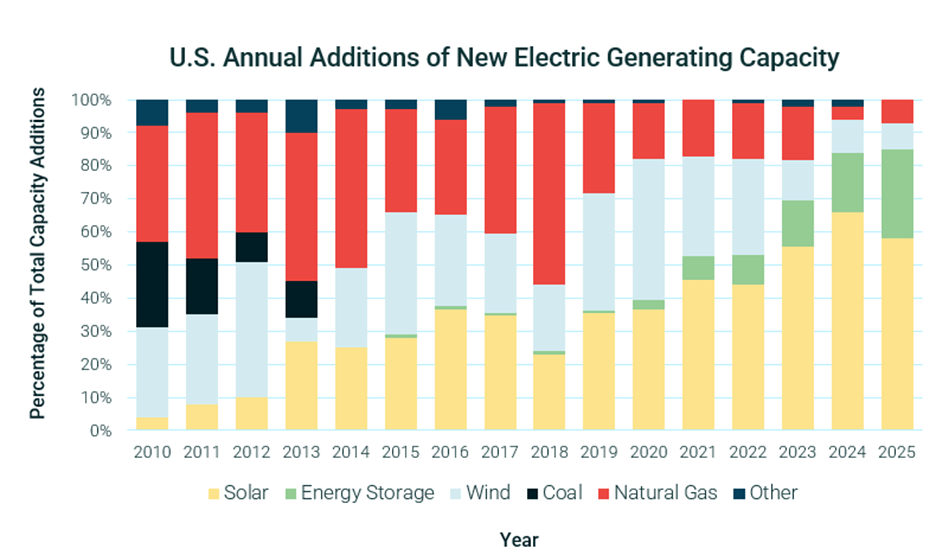

Renewables have grown from approximately 30% of annual new capacity additions in 2010 to 93% in recent years. In 2025, solar and storage combined accounted for 85% of new capacity additions, compared to 8% for wind and 7% for natural gas.

From a cost perspective, renewables remain highly competitive, even without tax incentives. From a timing perspective, speed to market is a major advantage. Technologies with long lead times may not be able to respond quickly enough to near-term load growth. Gas turbine lead times, for example, have stretched significantly in recent years with delivery times now up to 7 years. Repowering and life extensions offer incremental capacity but aren’t a long-term growth engine.

Energy delivered sooner has inherent economic value, particularly when buyers are solving for reliability and cost today.

Tax incentives still matter, but their impact often flows through pricing structures. If incentives were reduced broadly across the market, projects would still be built, but pricing would likely adjust upward across the sector. In that scenario, the impact would be borne most directly by offtakers and ratepayers.

Lydia Li

Director of Investment, Arevon

“I’m often asked whether renewable energy can move forward without tax incentives. The answer is yes, renewables are still competitive without tax incentives. The most recent levelized cost of energy reports confirm that on an unsubsidized cost per megawatt-hour basis, renewable energy remains the most cost-competitive form of generation. Combined with the fact that they are the fastest generation resources to deploy, I believe renewables will continue to play a central role in adding new power generation in the United States over the next decade.”

Joseph Santo

Managing Director of Investment, Arevon

“Arevon’s Investment team is looking beyond levelized cost of energy measures, assessing the locations where unsubsidized solar and storage will continue to be the most cost competitive form of reliable generation available. Well-sited competitive solutions that improve the reliability and affordability of our grid cut through the volatility in the market.”

Storage and Hybrid Projects Are Reshaping Grid Economics

Energy storage is increasingly central to grid planning and operations. Storage introduces dispatchability, which changes both the value proposition and the financing framework.

Arevon has deep experience across standalone storage and solar-plus-storage projects, and its forward strategy includes securing interconnection capacity for storage alongside utility-scale solar projects. The key value driver is often the capacity and dispatch flexibility storage provides to offtakers.

Corporates seeking around-the-clock solutions may value combined solar-plus-storage structures. Utilities may procure solar and storage separately, often based on localized transmission constraints and planning needs.

Market rules also shape outcomes. Some regions enable direct corporate procurement, while others require buyers to work through regulated utility structures. These differences influence contracting approaches and, ultimately, financeability.

In Closing: Financing the Grid America Needs for a Strong and Independent Energy Future

As the U.S. power system scales to meet rising demand, utility-scale solar and energy storage will remain central because they are cost-competitive, relatively fast to deploy, and can be structured to deliver predictable long-term value, including pricing structures insulated from fuel cost volatility. Project finance remains a key mechanism that makes that buildout possible. In today’s environment, the most financeable projects are those with strong contracts, disciplined risk management, and sponsors with the operational depth to navigate uncertainty over decades.

Denise Tait

Chief Investment Officer, Arevon

“Financing is ultimately a vote of confidence in the quality of the project and the strength of the team behind it. Arevon has built deep relationships with top-tier lenders and investors who recognize the bankability of our projects and the expertise across our platform. As a long-term owner and operator, we focus on building assets that perform reliably over decades. We believe being a good partner matters, not only to our financial counterparties, but also to the landowners and communities who host our projects.”

This is Arevon

Follow us on LinkedIn for more stories of how we’re powering progress.